Term Life Insurance Vs Whole Life Insurance

Life Insurance 101: Choosing the Right Policy for Your Needs

Life insurance can feel like a complex topic, but it doesn’t have to be. At its core, it’s a financial safety net for your loved ones. It ensures they receive a payout in case of your passing, helping them cover expenses and maintain their financial stability. But with various policy options and factors to consider, choosing the right life insurance can feel overwhelming. This guide will equip you with the knowledge to navigate life insurance with confidence.

The Two Main Players: Term Life vs. Whole Life

The life insurance landscape boils down to two primary categories: term life and whole life. Understanding these differences is crucial for making an informed decision.

-

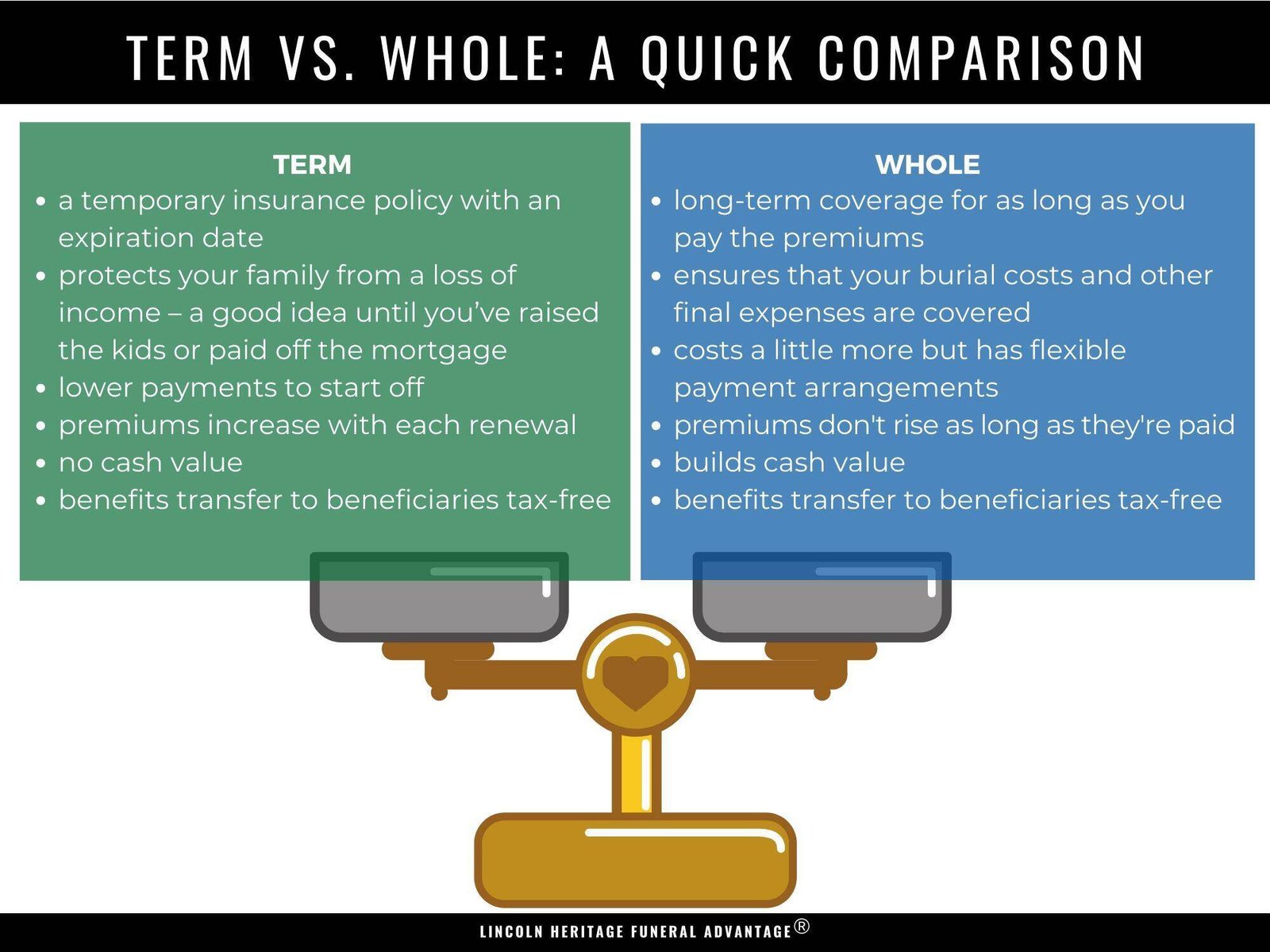

Term Life Insurance: Affordability and Simplicity

Term life insurance is like renting coverage for a specific period, typically 10, 20, or 30 years. It’s known for its affordability, making it a great option for those on a budget or needing coverage for a limited time, such as while raising children or paying off a mortgage. Here’s how it works:

* You pay a fixed premium throughout the term.

* If you pass away within the term, your beneficiaries receive a death benefit payout.

* However, if you outlive the term, the policy expires, and no payout is provided.

Term life is a straightforward and cost-effective way to ensure your loved ones’ financial security during a specific timeframe.

-

Whole Life Insurance: Coverage for Life (and a Savings Bonus)

Whole life insurance offers lifelong coverage, meaning it remains active until you pass away. It combines a guaranteed death benefit with a cash value component that grows over time. Here’s a breakdown:

* You pay a higher premium compared to term life.

* Part of your premium goes towards the death benefit, and the rest accumulates as cash value.

* You can access the cash value through loans or withdrawals (although this may reduce your death benefit).

* The cash value also grows with a guaranteed minimum interest rate.

Whole life offers long-term security and a potential savings element. However, the premiums are generally higher than term life.

Determining Your Coverage Needs: How Much is Enough?

Knowing how much life insurance coverage you need is essential. Here are some factors to consider:

- Dependents: If you have dependents who rely on your income, you’ll want enough coverage to replace your lost income and maintain their lifestyle.

- Debts: Consider outstanding debts like mortgages, student loans, or car loans. Factor in the amount needed to pay them off upon your passing.

- Future Expenses: Think about future costs like college tuition for children or elder care needs.

- Standard of Living: Estimate the amount your family would need to maintain their current standard of living without your income.

There are online life insurance calculators that can help you estimate your coverage needs. However, consulting a financial advisor can provide a more personalized assessment.

Factors Affecting Policy Premiums: Why Do Costs Vary?

The cost of your life insurance premium depends on several factors:

- Age: Generally, younger individuals pay lower premiums than older ones. The earlier you purchase life insurance, the more affordable it will be.

- Health: Your health status significantly impacts your premium. If you have pre-existing health conditions, you may pay a higher rate.

- Lifestyle: If you engage in risky hobbies like skydiving or smoking, your premium might be higher.

- Policy Type and Coverage Amount: Whole life insurance will have a higher premium compared to term life. Similarly, a higher death benefit will translate to a higher premium.

Additional Considerations: Riders and Exclusions

Life insurance policies can be customized with optional add-ons called riders. These riders provide additional benefits for an extra premium, such as:

- Disability Income Rider: Provides income if you become disabled and cannot work.

- Waiver of Premium Rider: Waives your premium payments if you become disabled.

- Accidental Death Benefit Rider: Increases the death benefit payout if your death is accidental.

It’s important to understand any policy exclusions that might limit coverage under specific circumstances, such as death by suicide within the first two years of the policy.

Shopping for Life Insurance: Getting the Best Deal

- Consider Independent Agents: Independent agents work with various insurance companies, offering you a wider range of options and potentially securing a more competitive rate. However, ensure they are licensed and have a good reputation.

- Ask About Health Questions: Be honest and upfront about your health during the application process. While some conditions may increase your premium, withholding information could lead to a claim denial later.

- Review the Policy Carefully: Before finalizing a policy, thoroughly read and understand all terms and conditions. Pay close attention to the death benefit amount, exclusions, and the process for filing claims.

The Bottom Line: Life Insurance for Peace of Mind

Life insurance is an investment in your loved ones’ future security. By considering your needs, budget, and the factors discussed above, you can choose the right policy that provides peace of mind knowing your family will be financially protected in your absence. Remember, a life insurance policy is a long-term commitment, so don’t hesitate to consult with a qualified financial advisor to navigate your options and ensure you make an informed decision.

Additional Resources:

- Life Happens: https://lifehappens.org/

- National Association of Insurance Commissioners: https://content.naic.org/

- The American College: https://www.theamericancollege.edu/

This comprehensive guide empowers you to make informed choices on your life insurance journey. Remember, there’s no one-size-fits-all solution. By understanding the different options and factors at play, you can secure the coverage that brings you and your loved ones peace of mind.